Staying Invested Through Geopolitical Shocks

Periods of geopolitical stress often create the strongest emotional pressure to act. When conflict escalates, oil prices move sharply, and markets turn volatile, investors can quickly feel that remaining patient is no longer enough. Yet these are often the moments when investment decisions benefit most from perspective rather than urgency.

In March 2026, the escalation involving the United States, Israel, and Iran unsettled markets and renewed concern about the economic consequences of geopolitical conflict. Oil prices have moved sharply, financial conditions have become more fragile, and investors are once again being asked to distinguish between short-term market stress and long-term portfolio impairment.

That distinction matters. Geopolitical shocks can be severe, and they should not be dismissed. But for long-term investors, the central question is rarely whether headlines are alarming. It is whether the event has changed the underlying purpose of the portfolio, the time horizon of the investor, or the discipline required to stay invested through uncertainty.

Why Investors Feel Pressured During Geopolitical Shocks

Geopolitical shocks create pressure because they compress time horizons. When conflict escalates, energy prices move sharply, headlines change quickly, and markets begin repricing growth, inflation, and policy expectations at the same time. Recent reporting on the March 2026 Middle East escalation shows that investors have been reassessing the risk of prolonged instability, higher energy prices, and broader macro disruption.

In that environment, the challenge often shifts from portfolio construction to emotional control. Short-term volatility can make even long-term investors feel that patience is no longer enough, especially when multiple asset classes respond differently and the usual sense of market stability begins to weaken.

That is why periods like this often feel more dangerous in real time than they appear in hindsight. The discomfort comes not only from the event itself, but from the difficulty of distinguishing between temporary repricing and lasting portfolio impairment while uncertainty is still unfolding. For long-term investors, that is often where discipline is tested most.

What History Shows in the Short Run

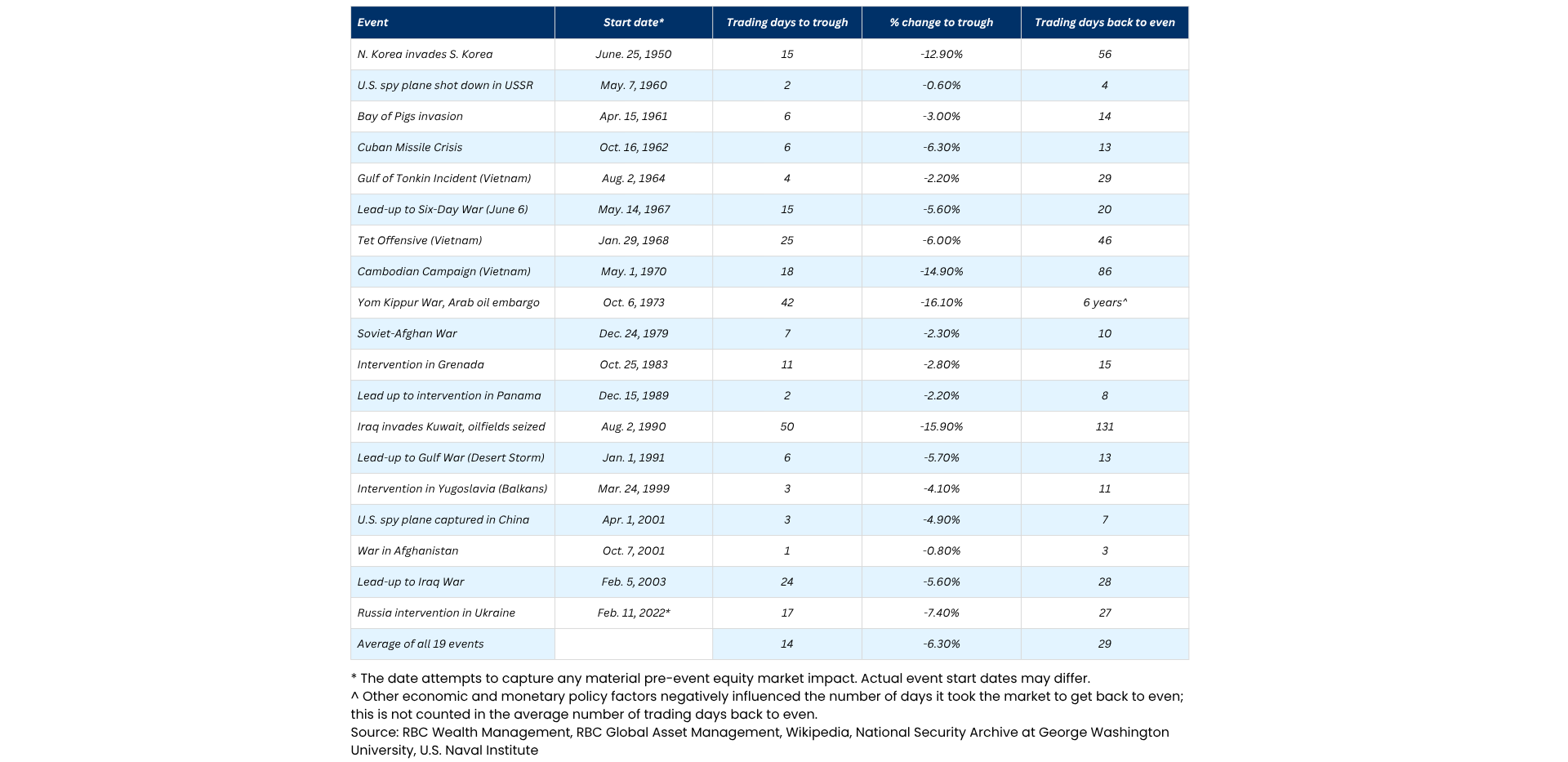

S&P 500 responses to select military interventions and hostilities since World War II

Short-term market declines during geopolitical shocks are not unusual, even when the headlines feel severe. RBC Wealth Management’s review of 19 major military interventions and hostilities since World War II found that the S&P 500 declined by 6.3% on average from peak to trough, reached its low after 14 trading days on average, and recovered to breakeven in 29 trading days on average.

That history should be used carefully. It does not mean every conflict follows the same path, nor does it guarantee that current markets will behave in line with the average. What it does show is that the initial market response to geopolitical shocks has often been sharp, emotionally uncomfortable, and shorter in duration than investors may fear in real time.

Oil-related shocks deserve added caution because they can affect markets through a broader macro channel. The 1973 oil embargo and the 1990 Iraq-Kuwait episode were among the more severe cases in RBC’s historical table, reminding investors that when conflict disrupts energy supply, drawdowns can be deeper and recovery periods longer

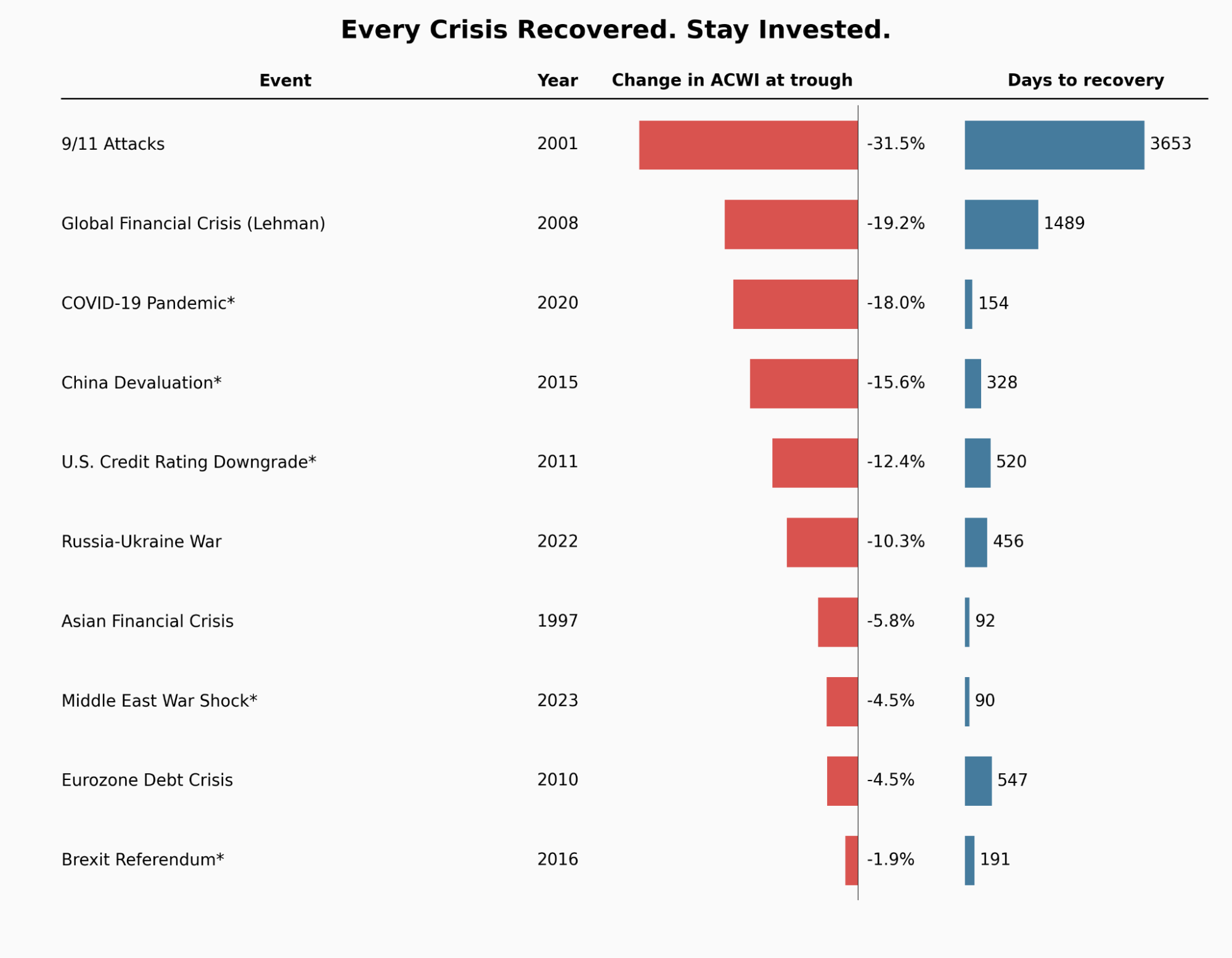

Why the Broader Global-Equity Perspective Matters

Short-run geopolitical-event studies are useful, but they do not fully reflect the experience of long-term global equity investors. A broader view shows that major shocks can produce very different drawdowns and recovery periods, depending not just on the event itself, but also on the policy response, liquidity conditions, and wider macro backdrop.

That is why a global-equity perspective matters. It helps move the discussion away from any single crisis pattern and toward a more realistic understanding that market stress is uneven, recovery paths vary, and long-term investing has always required endurance through periods that feel deeply uncertain in real time.

Replaced zero-change monthly baseline rows with yfinance daily maximum drawdowns ({patched_count} events) to correct temporal resolution disparities.

Drawdowns and recoveries reflect overlapping, unisolatable macroeconomic factors; event dates serve strictly as analytical anchors.

Sources: Metta Associates internal analysis based on an ACWI monthly proxy series and internally selected major-event dates. Drawdowns are measured from the pre-event peak to the trough, and recovery is measured as the number of calendar days required to regain the prior peak.

Our chart makes this clear. Crises with similar drawdown depth have produced very different recovery timelines, which suggests that the severity of a fall alone does not determine how long recovery will take.

The 9/11 episode is a good example. Its unusually long recovery period should not be read as a simple geopolitical template, but as a compounded case in which markets were still recovering when the Global Financial Crisis triggered a second major drawdown.

The key lesson is that recovery paths vary widely and can be extended by overlapping shocks. For long-term investors, that makes risk less a single-event problem than a question of duration, sequence, and the ability to remain invested through both.

What This Means for Long-Term Investors

For long-term investors, the main risk during periods like this is not only market volatility, but the temptation to abandon a sound strategy in response to it. Sharp drawdowns can feel like signals to act, even when they may prove to be temporary repricing rather than lasting impairment.

That is why the time horizon matters. A well-constructed portfolio is not built on the assumption that shocks can be avoided, but on the understanding that uncertainty, drawdowns, and uneven recoveries are part of long-term investing.

The more durable advantage is often not prediction, but discipline. Investors who remain aligned with their portfolio’s purpose are generally better positioned than those who allow short-term fear to redefine a long-term plan.

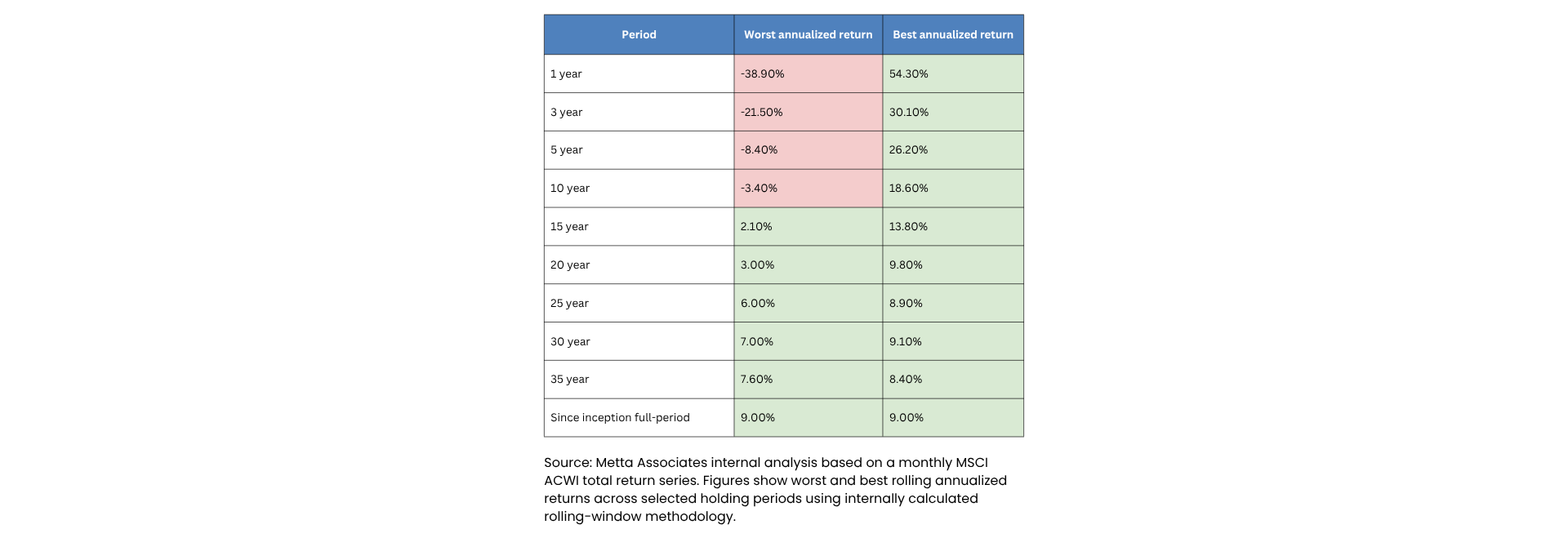

The table below shows how rolling annualized return outcomes have varied across different holding periods. The historical range is very wide over shorter horizons, but it narrows meaningfully as the investment period lengthens.

This pattern helps explain why long-term investing can feel so different from short-term market experience. Over one- and three-year periods, outcomes have historically been highly dependent on entry point and market conditions, while over longer horizons the range between worst and best outcomes has narrowed materially. That does not remove risk, but it does suggest that time has historically reduced the impact of poor timing and improved the stability of long-run outcomes.

Key Takeaways:

- Drawdown Does Not Predict Recovery: A deeper fall does not necessarily mean a longer recovery. Similar drawdowns have historically led to very different recovery timelines.

- Recovery Paths Vary Widely: Market shocks do not follow a single pattern. Outcomes depend not only on the event itself, but also on policy response, liquidity conditions, and the broader macro backdrop.

- Overlapping Shocks Extend Pain: The greater long-term risk is often a second shock arriving before the first recovery is complete. In practice, duration and sequence can matter as much as the original decline.

- Discipline Matters Most: For long-term investors, the biggest risk is often reacting emotionally to uncertainty. Time horizon, diversification, and process remain critical when markets feel most unstable.

Sources: Reuters; RBC Wealth Management; Metta Associates internal ACWI event and rolling-return analysis.

Metta Associates's Strategic Reflection

At Metta Associates, we believe periods like this test more than markets. They test the quality of a client’s planning, the resilience of their portfolio, and the discipline of the process supporting both. That is why our approach is built around globally diversified, multi-asset portfolio construction, structured financial planning, and long-term decision-making rather than reactive positioning around headlines.

This also reflects the values that guide our work. We believe stewardship requires prudence, clarity, and emotional discipline, especially when uncertainty is high. Our role is not simply to monitor markets, but to help clients remain anchored to a well-constructed strategy that aligns with their long-term objectives, liquidity needs, and tolerance for risk—always with you.

Disclaimer

The information presented is based on sources believed to be reliable; however, its accuracy or completeness cannot be guaranteed. This material does not represent a forecast and should not be interpreted as a guarantee of future outcomes. It has been prepared with care and objectivity to support long-term, planning-focused financial decisions.