Outlook 2026 The Great Realignment and Navigating Shifting Global Forces

The year 2025 represented a pivotal inflection point for the global economy, marking a systemic departure from a framework centered on cost efficiency toward a new paradigm anchored in national security and strategic resilience. This fundamental structural realignment was propelled by three defining catalysts.

A New Trade Order

Liberation Day marked a significant shift as the U.S. imposed the largest tariff hikes in a century. This spike in import costs pushed companies to order goods earlier than usual to avoid higher tariffs, leading to a sharp squeeze on retail margins. Consequently, companies pivoted from low-cost sourcing toward near-shoring and resilient supply chains, prioritizing national security and operational stability over mere price efficiency.

Fiscal Turbulence and the Information Vacuum

Fiscal tensions peaked with a record-breaking 43-day U.S. government shutdown as public debt surged past the nation’s total economic output. With limited official data available, investors were left in the dark, fueling sharp market swings. This uncertainty quickly spilled into the bond market, where investors began to question the government’s ability to manage its growing debt. As confidence weakened, bonds were sold off aggressively, pushing yields higher as investors demanded greater compensation for holding government debt that now appeared increasingly large relative to the country’s income and long-term fiscal stability.

The AI Revolution

2025 saw capital flood into physical AI as tech titans deployed unprecedented investment to move AI into tangible infrastructure, which includes data centers. This expansion pushed electricity demand to nearly double existing production capacity. The shift triggered a massive sector rotation. Capital migrated from traditional software companies that struggled to monetize toward energy and utilities. These sectors have emerged as the new backbone of the economy, essential for supporting a power- hungry AI future.

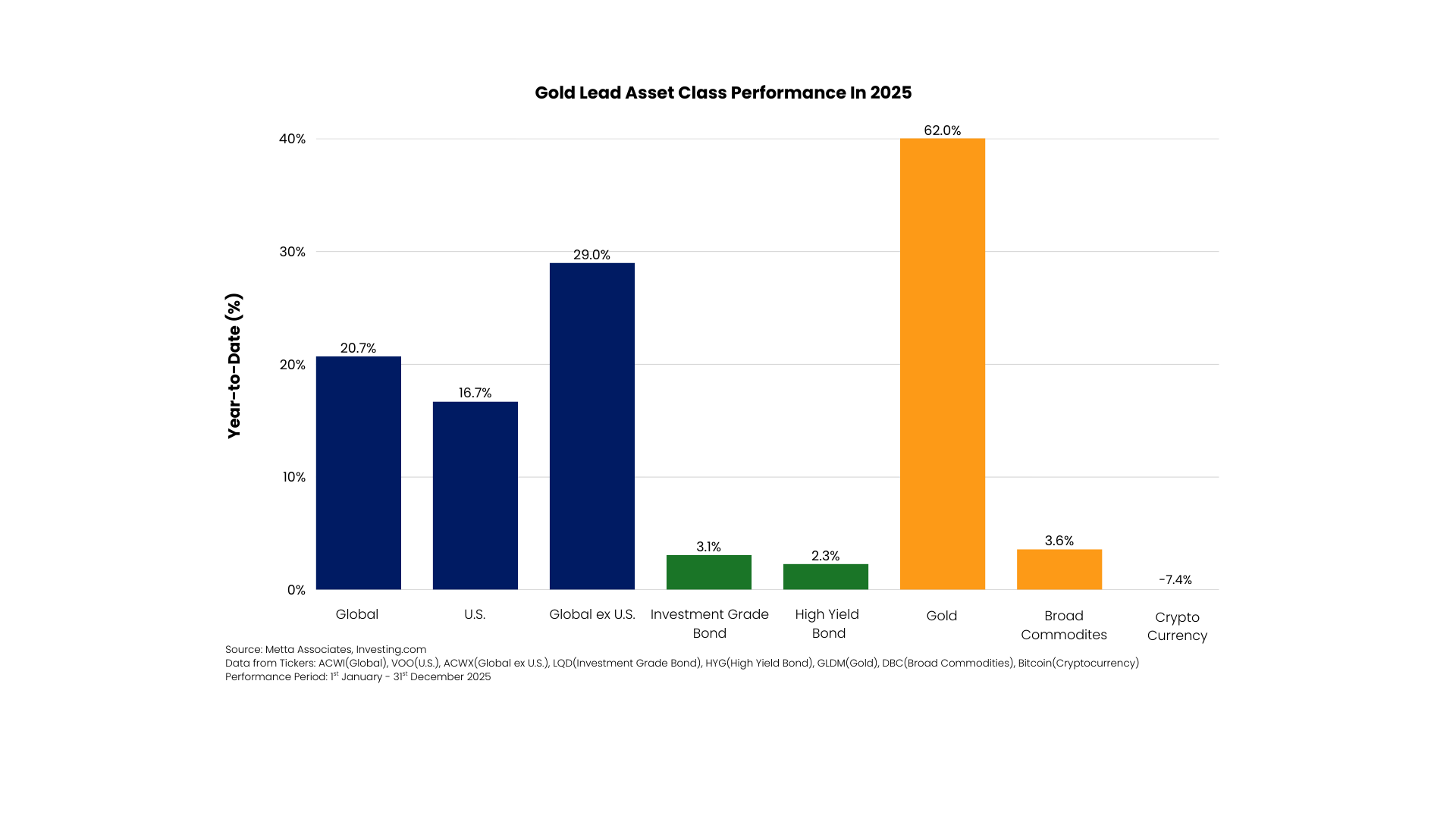

This mix of chaos and innovation led to remarkable returns across the board. Gold surged to an all-time high, delivering returns roughly three times higher than equities.. While U.S. equities advanced on the back of strong earnings, AI-driven innovation, and fiscal stimulus, this growth was highly concentrated in a small group of large technology companies. In contrast, global ex-U.S. markets delivered stronger overall performance, supported by a broader-based expansion across multiple industries and additional tailwinds from favorable currency movements.Having navigated this intense landscape, we now turn our focus to the new opportunities and strategies awaiting us in the 2026 Outlook.

To navigate such volatility, we reviewed 2026 outlooks from global banks, asset managers, and independent research houses such as J.P. Morgan, BlackRock, and UBS. then merged their views with our own analysis. The result is a concise synthesis of how shifting macro forces, valuations, and policy paths may shape risks and opportunities in 2026.

Three Forces are Likely to Define the Investment Backdrop in 2026

Turning AI Potential into Proven Profit

The AI landscape has matured from a period of conceptual hype into a tangible business era focused on infrastructure and measurable returns. This transition is being spearheaded by hyperscalers aggressively scaling their capital expenditure to expand data centers and secure latest-generation GPUs, a shift that continues to empower chip makers and power utilities while pressuring legacy software providers to adapt or face obsolescence. As the market shifts from building AI technology to actually making money from it, the biggest winners are no longer just the tech providers. Instead, companies in sectors such as finance, healthcare, and manufacturing are emerging ahead by using AI to reduce labor costs and improve day-to-day efficiency.

However, this momentum is not without risks. Beyond physical limits such as shortages of power and water, there are growing concerns about capital circulating within a small group of major players, where investment flows repeatedly between AI developers and their largest customers. This raises the risk that AI valuations may be overstated. If real profits fail to grow in line with the massive investment being made, the market could face the risk of an AI bubble forming.

How National Security Shapes the Market

Governments are increasingly prioritizing national security as a primary driver of economic policy, directing substantial capital toward infrastructure and defense to ensure long-term resilience. A pivotal element of this strategy is the One Big Beautiful Bill Act (OBBBA), signed in 2025. It is projected to serve as the primary engine of the U.S. economy in 2026, contributing a direct GDP boost of 0.5% to 0.7% through significant fiscal stimulus and liquidity injections. While this spending creates clear tailwinds for the construction, materials, and defense industries, the resulting surge in debt issuance exerts downward pressure on government bond valuations. The prevailing macro risk remains that elevated debt levels could sustain higher interest rates, ultimately challenging equity valuations as the market balances immediate economic momentum against long-term fiscal stability.

Prioritizing Security Over Cost

The world is shifting its focus from finding the cheapest costs to ensuring security and resilience in supply chains, driven by the U.S.-China competition and tightening trade policies. Notably, with the U.S. effective tariff rate expected to hit 15%-20% in 2026, there is a growing momentum toward onshoring and near-shoring to secure production lines despite the trade-off of higher costs. This shift favors North America and India as production moves closer to end markets, while China and Europe face much higher export costs. The resulting higher inflation floor stands as the primary risk, as domestic manufacturing remains costlier than traditional outsourcing.

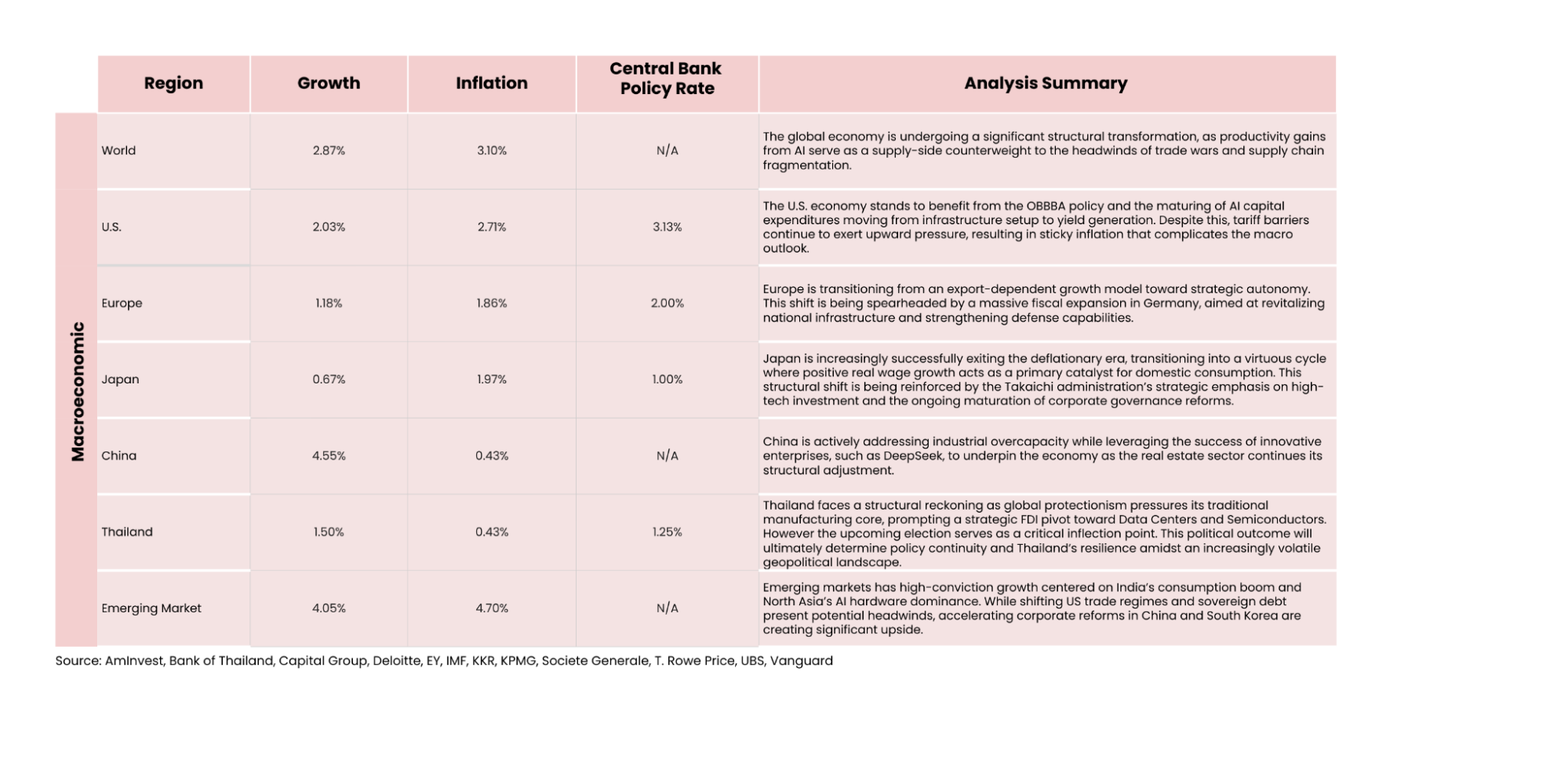

Macroeconomic

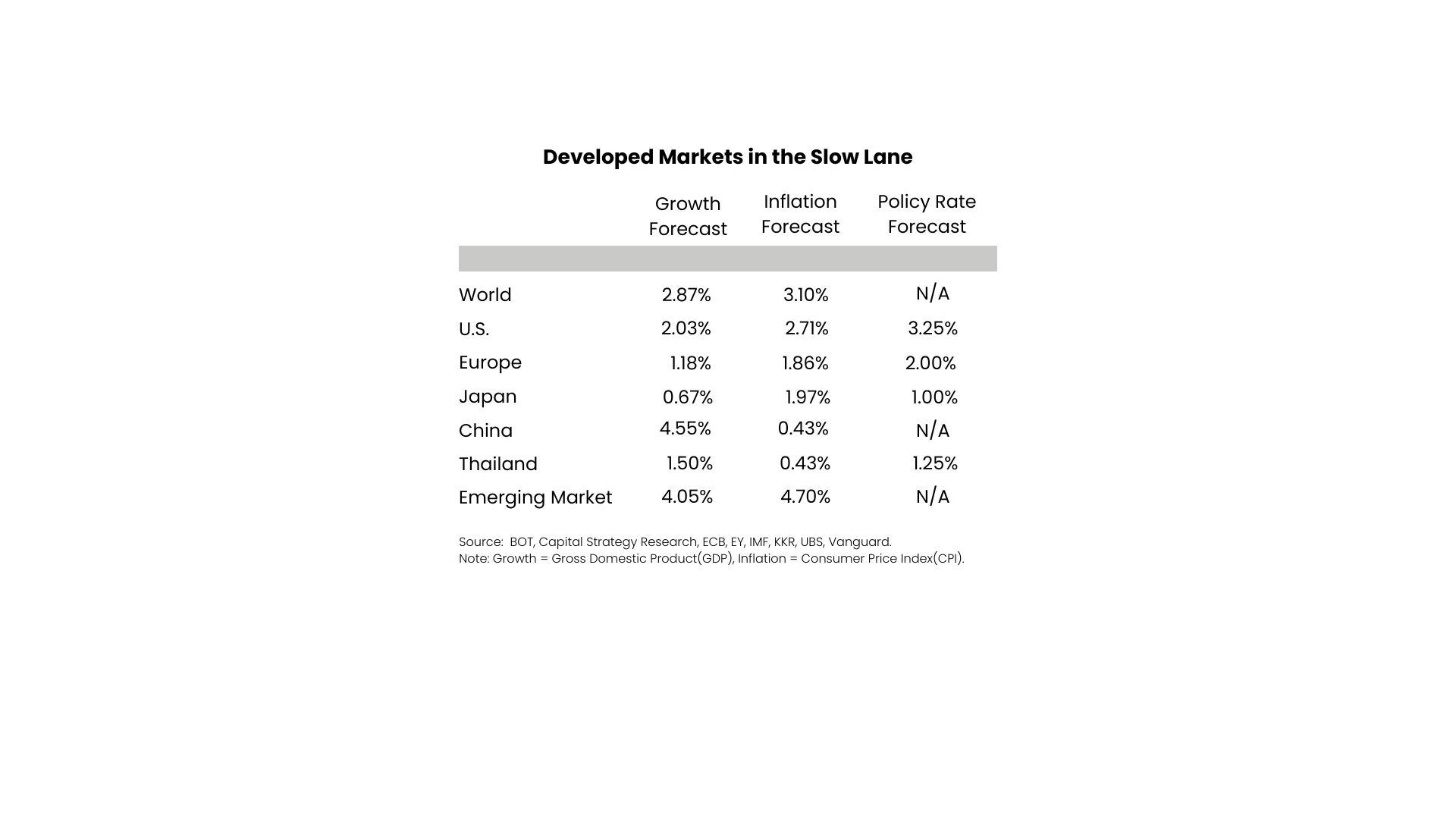

The U.S. remains the primary global growth engine, sustained by the fiscal tailwinds of the OBBBA stimulus. While this supports resilient GDP growth, the economy faces inflation that is over target, driven by trade tariffs and labor constraints, which is likely to keep the Federal Reserve’s neutral rates elevated, with scope for rate cuts toward the end of the year. However, the long-term trajectory is clouded by mounting public debt, which remains a critical structural risk for investors.

China is undergoing a high-stakes transition as it pivots from property-led growth toward new productive forces like AI, EVs, and green energy. While these sectors act as a buffer against deflationary pressures, the broader recovery is tempered by sluggish domestic demand and trade tensions. China's success in 2026 depends on balancing domestic regulation with the need to restore international investor confidence.

In 2026, Thailand faces a structural reckoning as global protectionism and trade shifts intensify pressure on its traditional manufacturing core. Amidst this transition, a strategic FDI pivot is gaining momentum, marked by successful inroads into high-value sectors such as data centers and semiconductor supply chains. However, the sustainability of this technological leap depends on the upcoming general election, which stands as a critical inflection point. The outcome will be the ultimate arbiter of policy continuity, determining Thailand’s ability to solidify these investment gains and navigate an increasingly volatile geopolitical landscape.

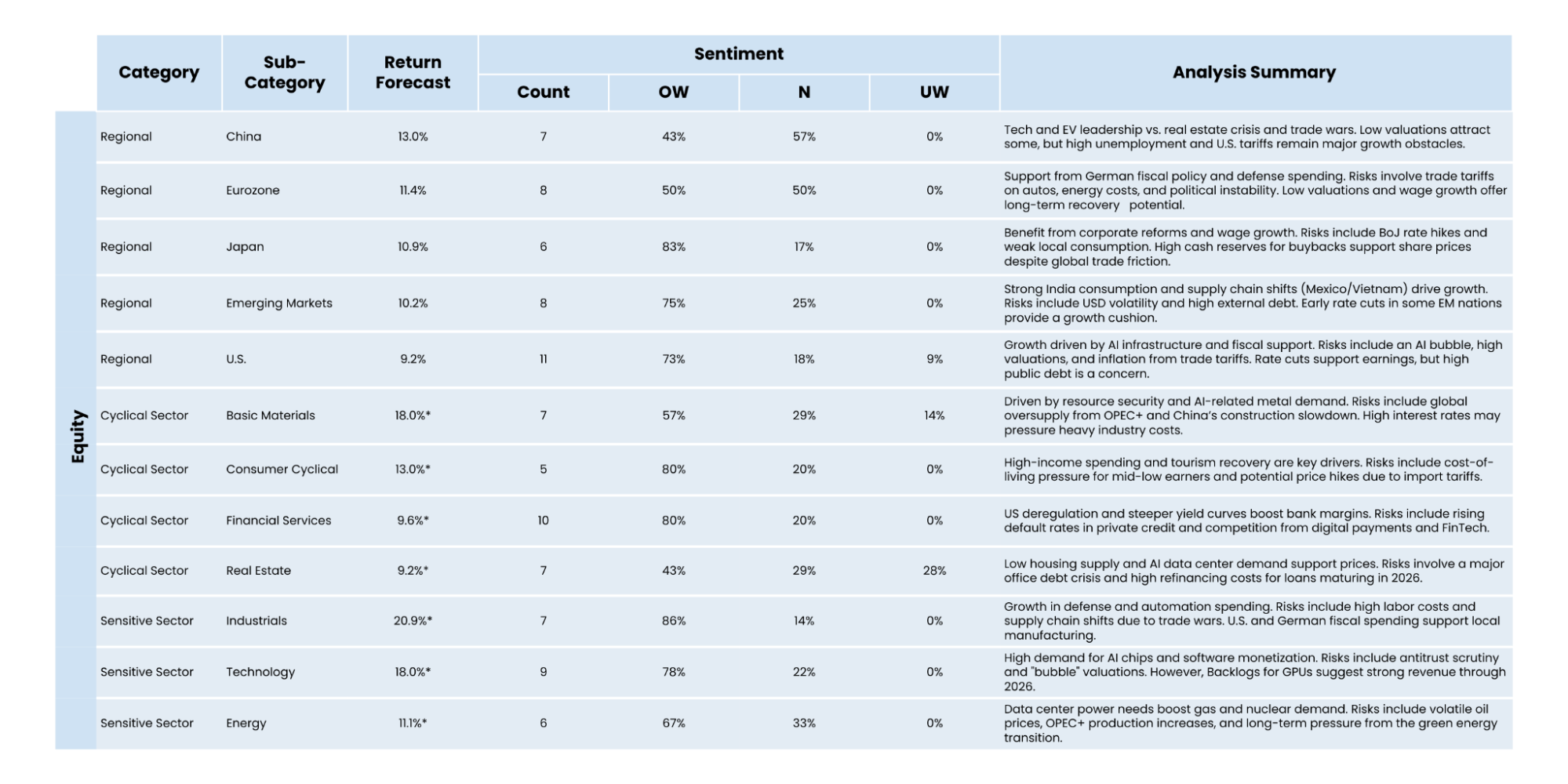

Asset Class

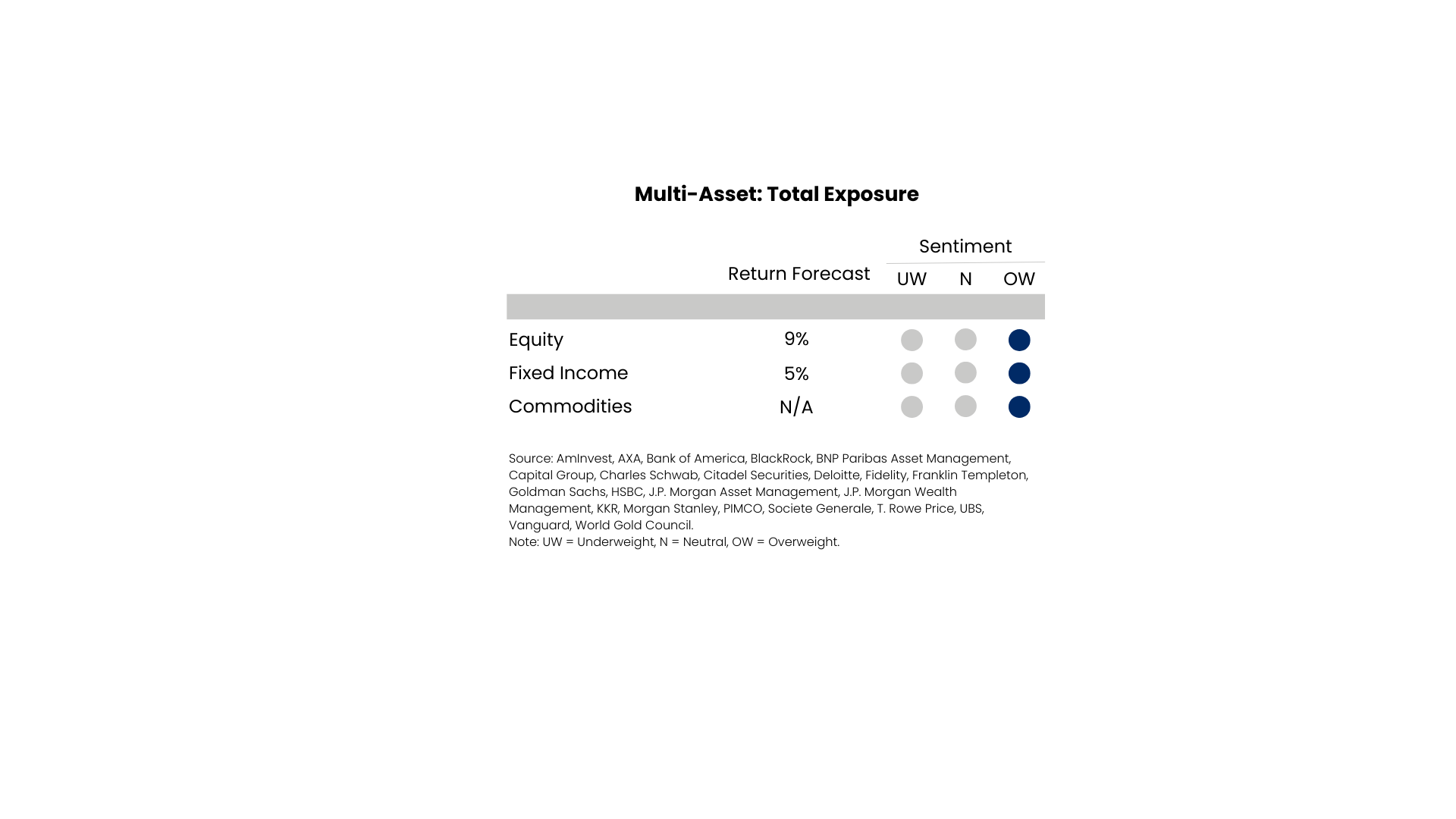

The 2026 outlook is generally positive for equities, with many large investors expecting growth to extend beyond a small group of technology leaders and show up across more sectors. This view is supported by continued investment in AI infrastructure such as data centers, energy, and networks as well as ongoing government spending that helps support economic activity. Together, these forces are expected to drive healthier and more widespread earnings growth. At the same time, commodities are gaining importance: gold is seen as a safeguard against geopolitical uncertainty and policy surprises, while industrial metals matter because technological growth ultimately depends on real-world inputs like energy and raw materials.

Fixed Income, however, are viewed more cautiously. While current yields are attractive and worth locking in, large government deficits could keep interest rates higher and lead to more price swings. As a result, many investors are becoming more selective with their fixed income holdings while limiting risk. A key change for 2026 is that equity and fixed income may move more closely together than in the past, reducing their ability to balance each other.

Equity

Regional

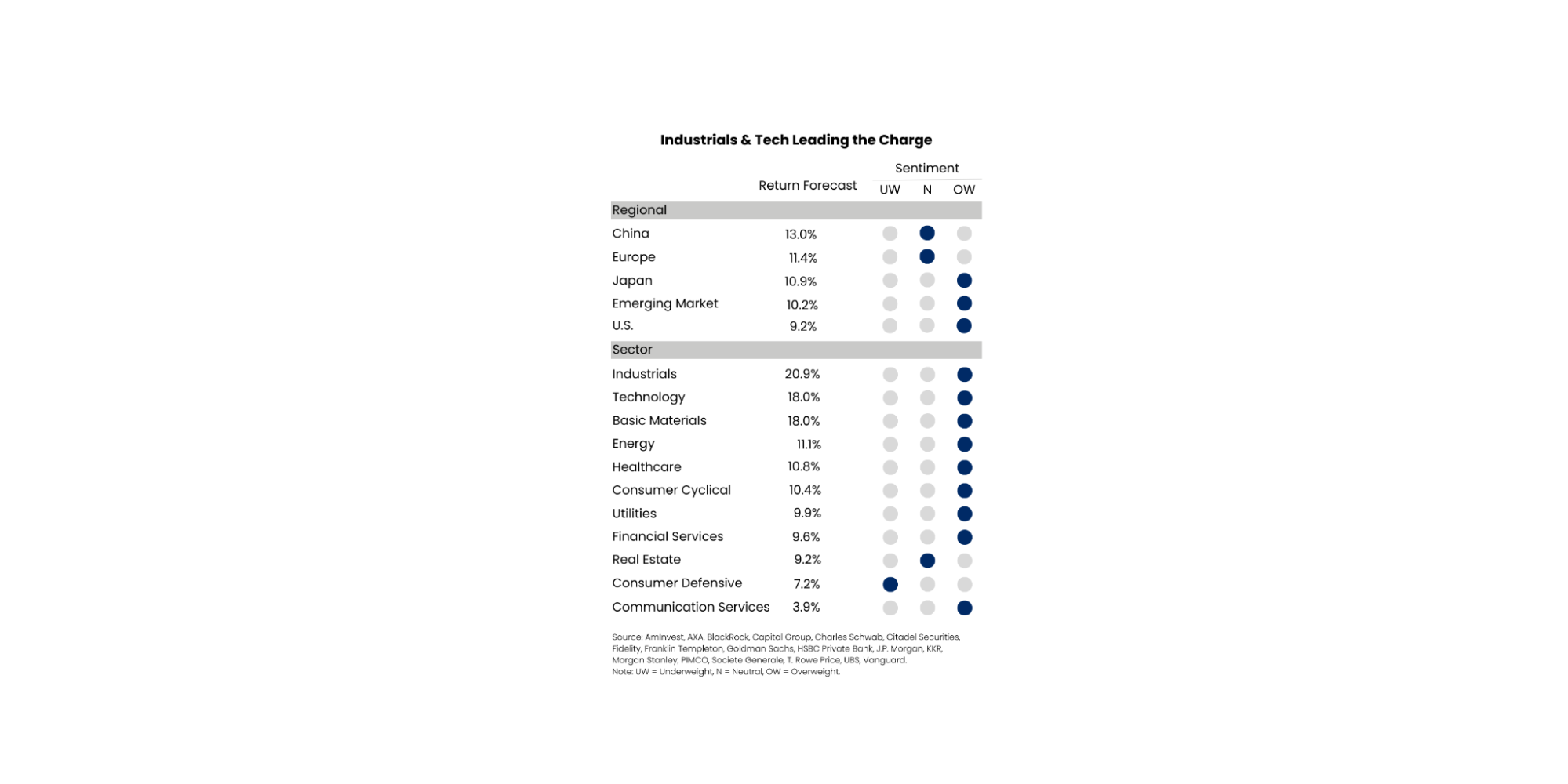

As we venture into 2026, the U.S. equity market is transitioning into a high-conviction era of AI monetization, where financially strong balance sheets allow industry leaders to translate technological innovation into tangible bottom-line efficiency. This structural tailwind is further amplified by a massive liquidity injection from the OBBBA tax refunds, providing a robust fiscal cushion as the year begins. Parallel to this, emerging markets are redefining their role as the indispensable backbone of global trade. China+1 (diversifying production beyond China to mitigate supply chain and tariff risks) and near-shoring trends have matured into a powerful engine of growth, positioning India as a preeminent hub for service-led expansion. Simultaneously, strategic hubs like Mexico and Vietnam continue to reap the rewards of a fundamental global production reshuffle, fortifying their structural resilience and cementing a new era of regional prosperity.

Sector

Heading into 2026, the equity narrative is defined by a powerful synergy between the technology and industrial sectors, which are acting as twin engines of long-term structural growth and shaping the next phase of market leadership. The technology sector is moving beyond speculative infrastructure investment into a high-confidence monetization phase, where the adoption of agentic AI is delivering measurable returns across software platforms and shifting the focus toward profitability and efficiency.

At the same time, the industrial sector has evolved beyond its traditional cyclical role to become a core pillar of national security and economic independence. This shift is driven by accelerating global reshoring and sustained government spending, leading to a multi-year expansion in defense, infrastructure, and strategic security investment. Crucially, industrial capabilities, particularly in power management and advanced cooling systems, now provide the physical foundation required for AI-driven digital growth, creating an integrated ecosystem of infrastructure and intelligence that defines market leadership as we move into 2026.

Conversely, Consumer Staples is now the least favored sector, burdened by eroding pricing power and an inability to pass through rising costs from tariffs and near-shoring. With capital rotating toward fiscal-driven infrastructure and AI growth, the sector faces a persistent margin squeeze and high opportunity cost, struggling to compete with the structural efficiency gains defining the new market leaders.

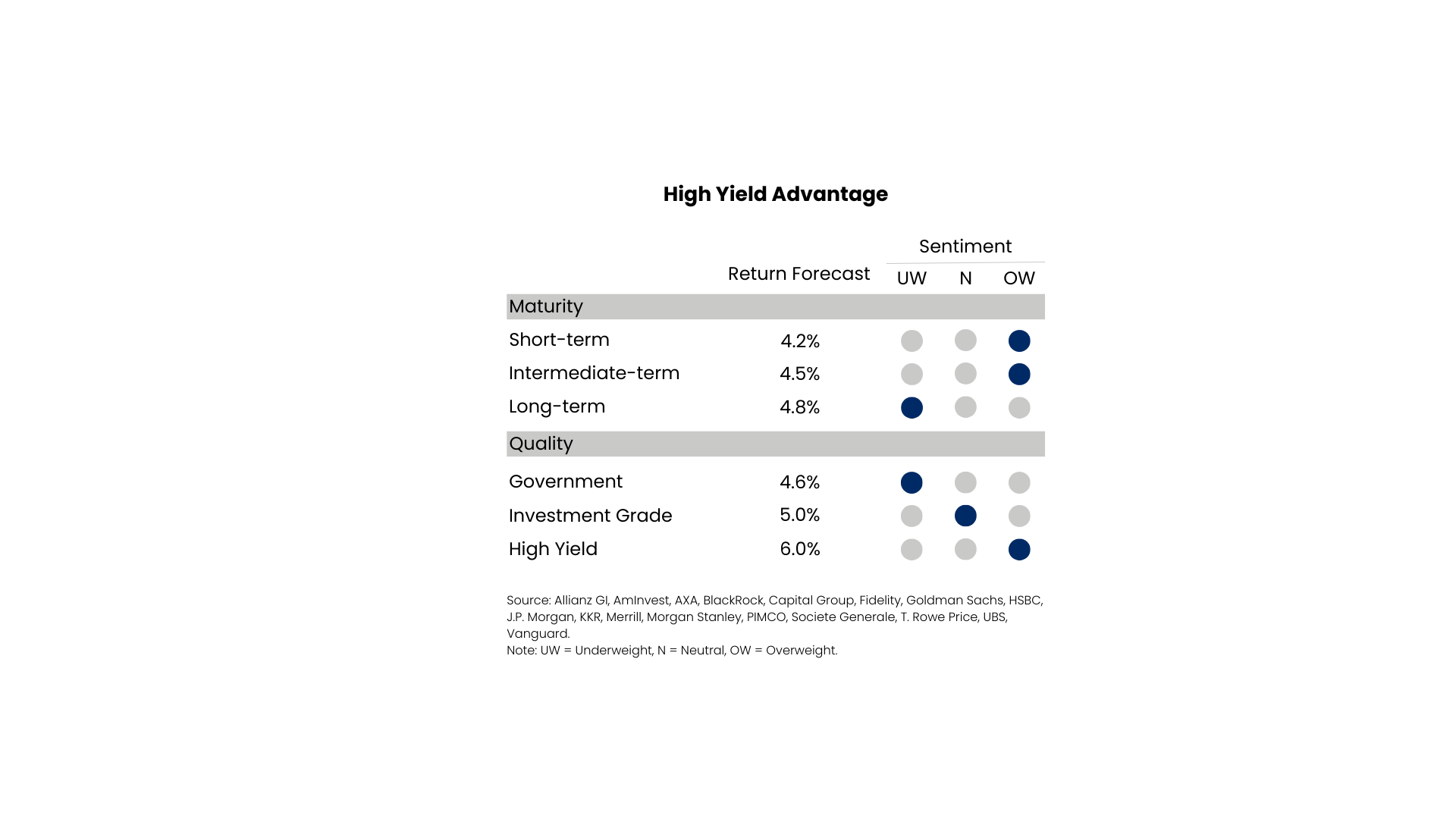

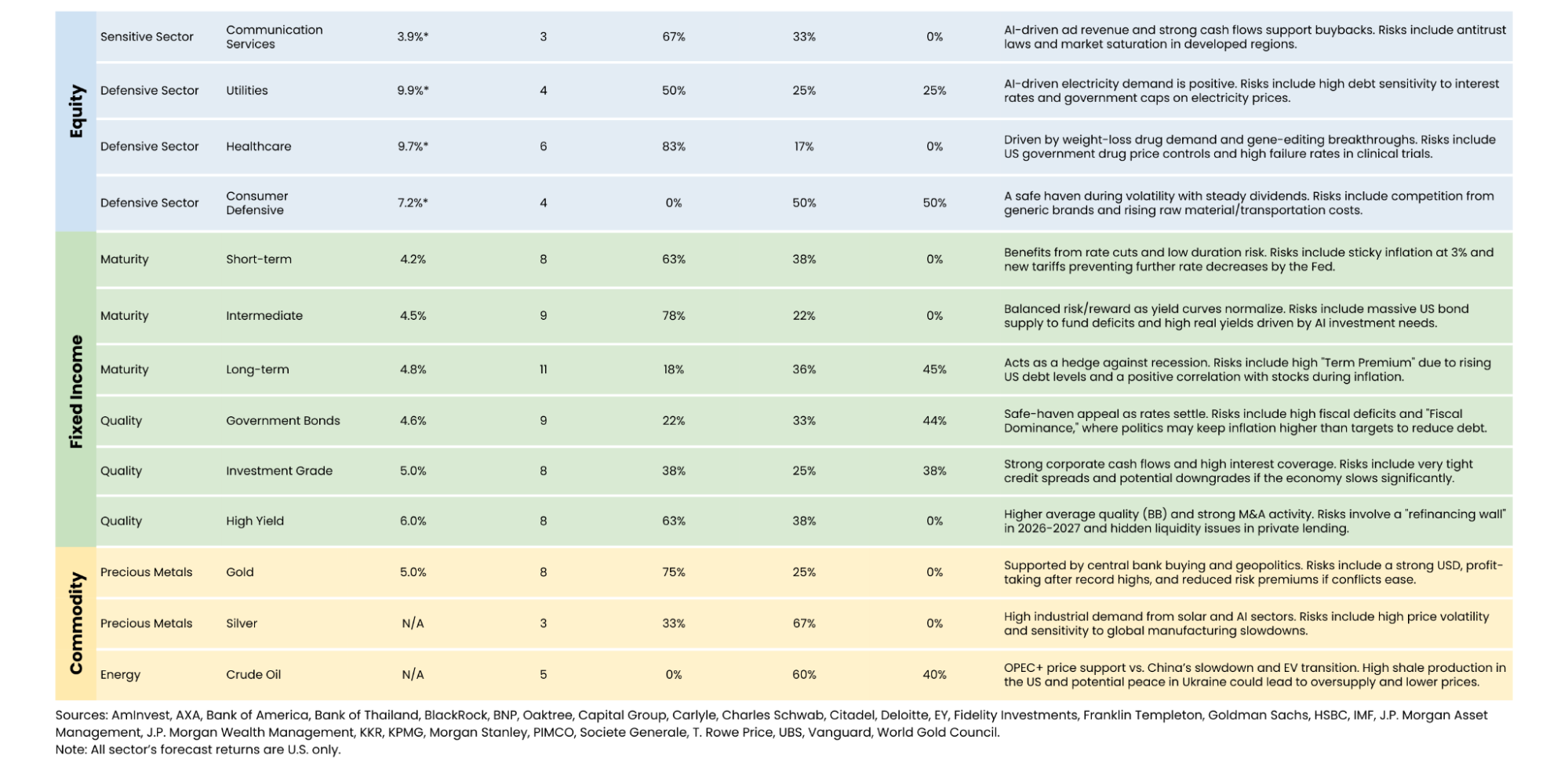

Fixed Income

The 2026 global fixed income landscape has transitioned from interest rate volatility to a dedicated pursuit of sustainable cash flow. The first standout flagship is the intermediate-term segment, the strategic sweet spot as investors pivot away from long-term pressure by fiscal discipline concerns and an oversupply of government securities, choosing instead to lock in yields within a manageable risk framework.

Concurrently, the second key flagship is the strategic embrace of high yield, underpinned by robust economic resilience and lower-than-expected default risks. This confidence allows investors to prioritize credit spreads as the primary engine for total return, moving beyond a passive reliance on capital gains from falling rates and toward a more proactive, yield-driven strategy that captures the strength of the real economy.

Commodities

Precious Metals

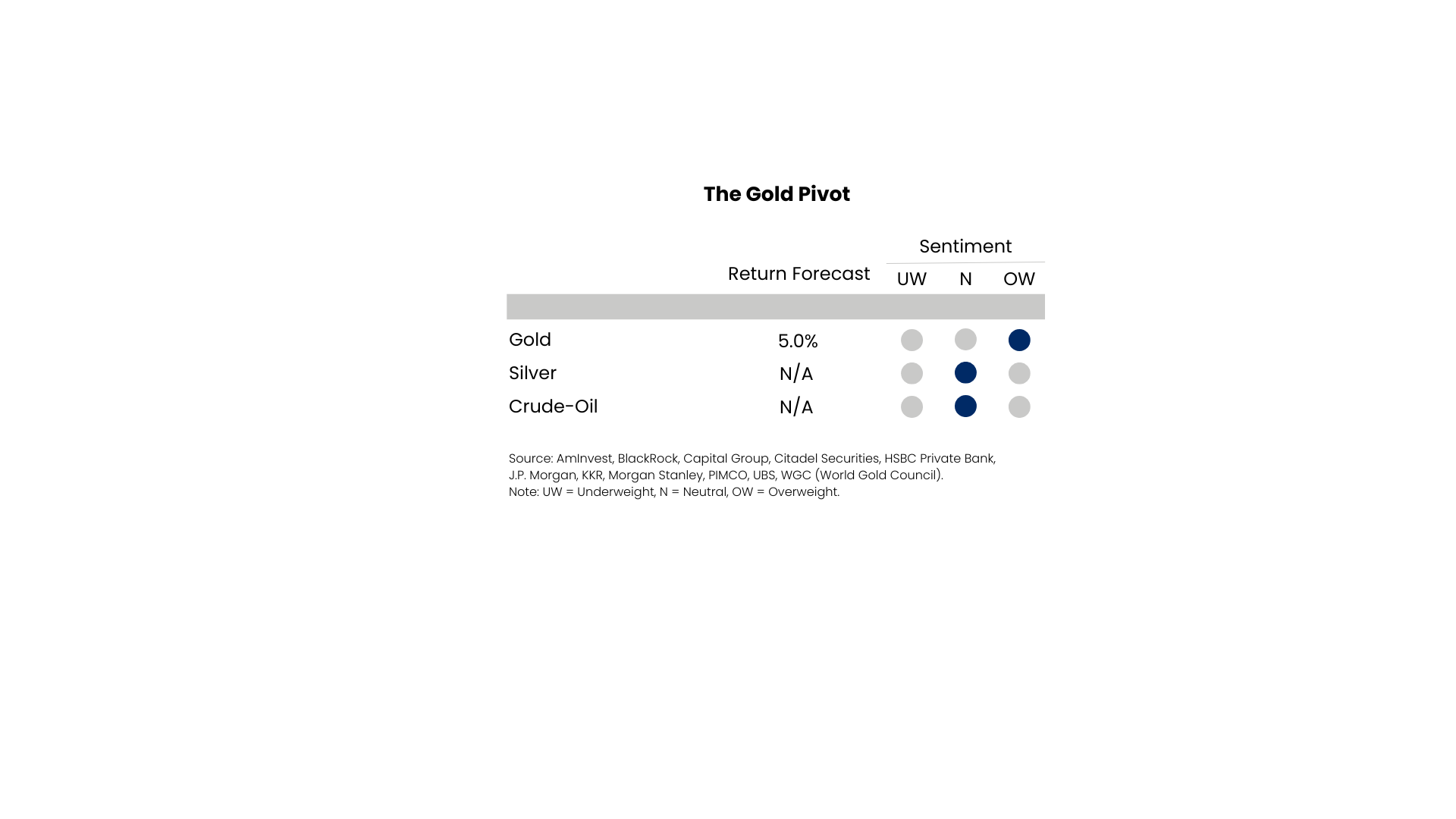

In part of commodities, gold is largely shaped by concerns over governments’ ability to sustain rising debt levels and maintain fiscal discipline. As a result, gold continues to play a key role as a hedge against expanding public debt and a global monetary policy environment that is settling into a new balance. In contrast, silver is increasingly viewed as a critical industrial metal supporting the expansion of AI technologies and the transition to clean energy. However, its performance is influenced by opposing forces, strong industrial demand on one side and a macroeconomic backdrop that remains only partially supportive on the other. This dynamic highlights a growing split within the metals space: gold remains centered on capital preservation, while silver’s performance is more closely linked to the pace of technological and industrial growth.

Oil

For crude oil, the market is confronting long-term fundamental changes in the market rather than a temporary price cycle. The main downward pressure comes not only from rising output by non-OPEC+ producers but also from a significant shift in demand behavior. Most notably in China, the rapid adoption of electric vehicles and alternative energy sources is beginning to have a lasting impact on crude oil consumption. As a result, the 2026 market has become a battleground between producers competing for market share and a global economy that is steadily reducing its reliance on fossil fuels, leaving oil in a challenging position amid multiple, persistent pressures.

Agreement & Controversies

Agreement

From AI Hype to Infrastructure & Monetization: The artificial intelligence narrative has matured into its second phase, transitioning from software-centric models toward physical AI and tangible infrastructure. Hyperscalers are accelerating capital expenditure with a renewed focus on realizing concrete monetization and driving measurable productivity gains across industrial and corporate sectors.

Global Monetary Normalization: A significant transition is underway as major central banks steer policy toward a neutral rate expected to stabilize around the 3.0-3.3% range. This pivot signifies the end of the cash-dominant era. As liquidity yields diminish, institutional capital is migrating toward risk assets and intermediate-duration fixed income to capture more sustainable returns.

The Security of Everything: The global economic paradigm has shifted from cost-efficiency to supply resilience. Strategic priorities now favor sectors poised to benefit from reshoring and friend-shoring initiatives.

Japan’s Corporate Renaissance: Japan stands out as a primary strategic focus within developed markets. Driven by Sanaenomic, a combination of fiscal stimulus and rigorous corporate governance reform, the nation is successfully unlocking value through improved capital efficiency. The focus on increasing return on equity and redistributing excess balance sheet cash marks a secular turning point for the Japanese market.

Procyclical Fiscal Impulse: Global growth in 2026 is being anchored by a synchronized wave of fiscal expansion. From the tax-relief mechanisms of the OBBBA in the United States to Germany’s commitment to large-scale infrastructure renewal, these fiscal engines are providing a crucial backstop, ensuring a recovery for the global economy.

Controversies

The Sustainability of AI Capital Expenditure: Debate persists over whether current spending represents an existential investment for long-term survival or a cycle clouded by circular financing and diminishing returns. The core uncertainty remains whether this capital intensity will drive a new era of productivity or culminate in a traditional market bubble.

Inflation Dynamics and the Neutral Rate: A tug-of-war exists between the inflation that remains persistent due to tariffs driven by tariffs and the disinflationary AI view, which anticipates that productivity breakthroughs will allow central banks to ease policy more aggressively than current market pricing suggests.

The Destiny of the US Dollar: The greenback’s trajectory is contested by a bearish narrative of yield convergence and a multipolar world versus the U.S. exceptionalism perspective, which argues the dollar remains the indispensable operating system of the global economy with no viable alternative.

The Role of Fixed Income: Institutional sentiment is split between viewing fixed income as essential risk ballast and a reliable source of carry versus a more defensive stance triggered by mounting public debt levels and the potential erosion of the traditional fixed income-equity correlation.

Weighing China's Policy Potential Against Structural Risks: The outlook remains highly divided, balancing the short-term investment potential from policy adjustments and advances in high-technology sectors against ongoing structural challenges, including property-sector stress and continuous deflationary pressures.

Key Takeaways

Synergy of AI Monetization and Physical Infrastructure

The AI landscape has shifted from hype toward physical AI where technology and industrials act as interdependent growth engines. Capital is aggressively scaling toward data centers and power utilities, prioritizing measurable monetization and operational efficiency over speculative software build-outs.

Security and Resilience over Cost

Global policy has pivoted from a singular focus on cost-efficiency toward national security and economic resilience. Governments now view supply chains not just as a business decision but as a strategic asset. As a result, policies increasingly encourage onshoring and near-shoring, aiming to reduce dependence on geopolitically sensitive regions and minimize the risk of sudden disruptions.

This shift reflects lessons learned from recent shocks, trade conflicts, pandemics, and geopolitical tensions which exposed the vulnerability of overly concentrated global supply chains. While this approach may raise short-term costs, policymakers are prioritizing reliability, control, and continuity of production over marginal cost savings. Over the long run, this transition is reshaping global trade flows, investment patterns, and corporate strategy, with countries offering incentives to attract manufacturing capacity and critical industries back within trusted borders.

OBBBA as the Primary Engine of the U.S. Growth

The OBBBA serves as the central catalyst for the U.S. economy. While this fiscal stimulus anchors growth in construction and defense, the resulting debt surge exerts downward pressure on bond valuations and challenges long-term fiscal stability.

Metta Strategic Reflection

2025 Market Performance & Portfolio Resilience

In 2025, gold dominated headlines with a remarkable surge of over 60.0%. However, these gains were accompanied by extreme volatility and a high price for those unprepared. While global equities faced an -18.4% drawdown and commodities plunged by -37.4%, our simulated multi-asset portfolio (60% Equities, 35% Fixed Income, 5% Gold) demonstrated its true resilience.

By delivering a 20.0% return and limiting maximum losses to just -11.6%, the strategy proved its worth. At Metta Associates, we view this as a vital reminder: chasing performance without a balanced framework creates unsustainable risk—especially for wealth intended for your near-term milestones.

Lessons from the Tariff Shock: Discipline over Emotion

The necessity of discipline was vividly illustrated during the "Tariff Shock" in early April 2025. News of new tariffs triggered a wave of panic selling, erasing 9%–11% of market value in just two days. While many investors reacted emotionally, fearing a deeper crisis, the downturn proved short-lived. As anxiety subsided, the market staged a sharp single-day recovery, reclaiming much of what was lost.

This episode offers a crucial lesson for long-term investors: short-term market drops are often fueled by sentiment rather than shifts in fundamentals. Those who sold during the dip merely locked in their losses and missed the rebound. In contrast, those who remained disciplined were positioned to benefit fully when prices bounced back.

The Metta Approach: Stability Through Personalization

Ultimately, we believe true stability is rooted in personalization, not in speculating on a single market outcome. By tailoring strategies to your unique time horizon and risk tolerance, we ensure your portfolio is engineered to thrive in any scenario.

This bespoke approach allows Metta Associates to transform market uncertainty into long-term security, keeping your financial journey in harmony with your goal.

Always with you.

Appendix:A

Appendix: B

Disclaimer

This content is intended for general informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instruments. It does not consider your specific investment objectives, financial situation, or needs. You are encouraged to consult a licensed financial advisor before making any financial decisions.