Staying Rich Together – Why a Dedicated Family Office Outlasts Fortune Alone

When oil magnate J. Paul Getty died in 1976, his personal fortune exceeded US $6 billion—then the largest in the world. Yet, within two generations the family's wealth splintered through litigation, lifestyle excess, and conflicting priorities. Art masterpieces were sold to pay estate taxes, heirs battled in court, and external advisers worked in silos. Getty's heirs were wealthy by any measure, but the absence of a unifying system—one that combined transparent governance, technical planning, and shared accountability—proved costlier than any market drawdown.

Getty's story isn't unique. It reveals a systemic problem affecting wealthy families worldwide.

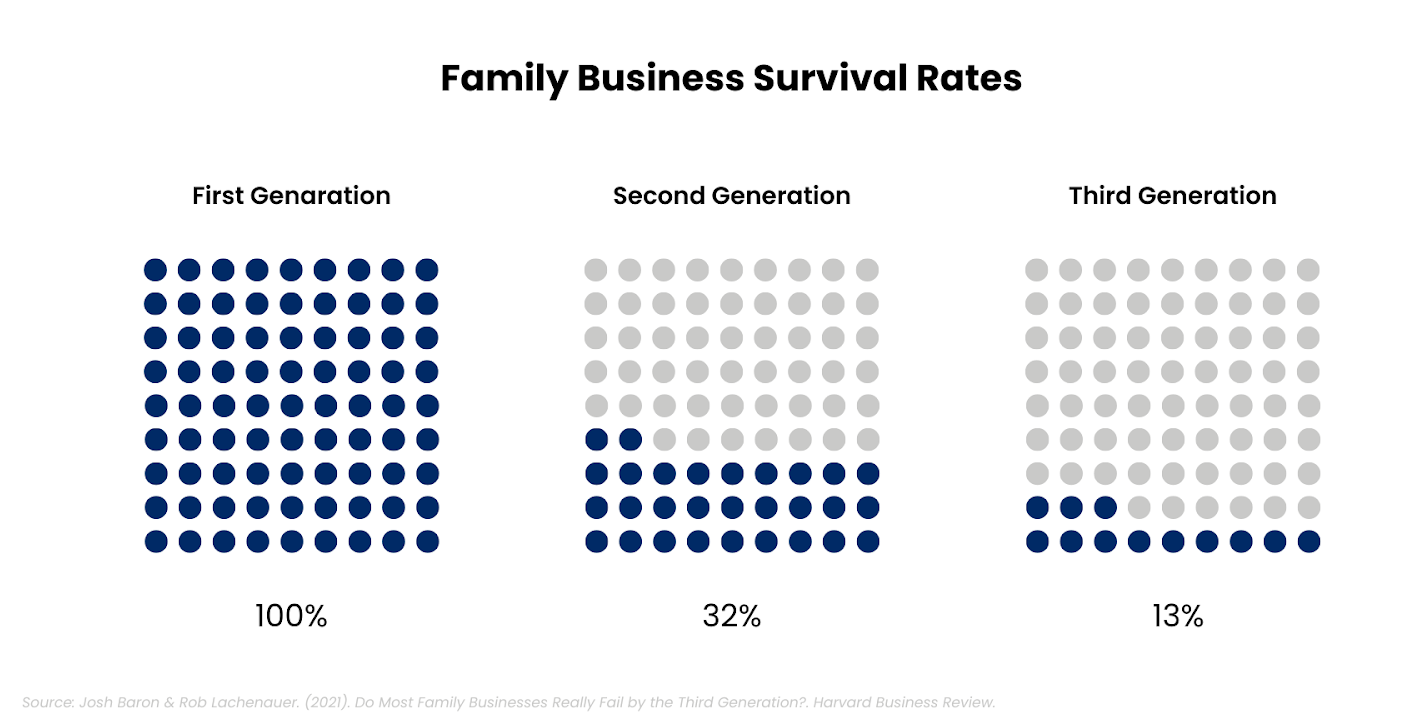

Recent research shows that 87% of family fortunes disappear by the third generation. The culprit isn't market crashes or bad investments—it's poor family systems.

According to UBS Global Family Office Report 2024:

70% of families say their biggest risk is "internal dynamics, not markets"

Only 32% have formal governance rules for decisions and disputes

Most families rely on fragmented advice—separate advisers for investments, taxes, and estate planning. When these advisers don't communicate, opportunities vanish and conflicts multiply.

The evidence for change is compelling. Deloitte's Report reveals that single family offices worldwide have surged from 6,130 in 2019 to 8,030 today—a remarkable 31% increase in just five years. This growth accelerates dramatically, with projections reaching 10,720 family offices by 2030, representing a 75% increase over the decade. Alongside this institutional growth, the total wealth managed by these families has expanded from US$3.3 trillion in 2019 to US$5.5 trillion today, with expectations to reach US$9.5 trillion by 2030.

This explosive growth isn't coincidental. It reflects families' growing recognition that lasting wealth preservation requires more than investment returns—it demands integrated systems designed for multi-generational stewardship.

But what exactly makes a Family Office approach so different from traditional wealth management? The distinction comes down to integration versus fragmentation.

What a Family Office Does Differently

Most wealthy families work with multiple advisers—one for investments, another for tax planning, a third for estate matters. But when advisers don't talk to each other, opportunities get missed and conflicts arise. A Family Office eliminates these gaps by putting all your financial needs under one roof, with one team that knows your complete picture.

However, simply consolidating services isn't enough. What truly distinguishes successful Family Offices are the foundational principles that guide their operations day after day.

What Keeps a Family Office Strong

Clear Rules, Shared Vision A simple family charter spells out who decides what, how disagreements are handled, and what the money is really for. It keeps everyone rowing in the same direction.

One Big Picture of the Money All assets—businesses, properties, trusts, even art—show up on a single dashboard. When you can see everything together, risks and opportunities are obvious instead of hidden.

Teach the Next Generation Early Heirs sit in on planning meetings long before they inherit. With guidance from seasoned advisers, they gain the skills and confidence to steward wealth—not just spend it.

Conversations That Go Beyond Returns Quarterly “family huddles” focus on goals, values, and life changes first, investment numbers second. Money then serves the plan, not the other way around—and our promise of always with you becomes real.

Taken together, these principles show that a Family Office isn’t just about services—it’s about creating a durable system. To see why they matter so much, let’s distill them into the key lessons every family should remember.

Insurance payouts, heroic investment returns, or elite private-bank teams alone cannot guarantee permanence. Without an integrated system, the next generation inherits assets but not the wisdom to manage them, and advisers struggle to serve shifting goals.

Key Takeaways:

Wealth tends to vanish—systems endure 87%of fortunes erode by the third generation without formal governance.

Transparency + Education + Accountability is the three-legged stool; remove any leg and stability fails.

Early heir involvement converts entitlement into stewardship, turning “my inheritance” into “our legacy.”

Ask whether your current adviser set-up can deliver this system not just returns—before another generation passes.

Sources: UBS, Deloitte, Campdenwealth, Harvard Business Review

Metta Associates's Strategic Reflection

At Metta Associates we view wealth as a long-term enterprise, not a short-term portfolio. Our role is to help families build the in-house office they deserve—whether through full family-office oversight or by integrating missing pieces (governance charters, consolidated reporting, heir education) into existing relationships. If your current advisers focus only on performance snapshots or product recommendations, it may be time to rethink whether the right framework is in place. Stewardship demands more than returns; it requires structure, dialogue, and continuous care

Always with You.

Disclaimer

This content is intended for general informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instruments. It does not consider your specific investment objectives, financial situation, or needs. You are encouraged to consult a licensed financial advisor before making any financial decisions.

The information presented is based on sources believed to be reliable; however, its accuracy or completeness cannot be guaranteed. This material does not represent a forecast and should not be interpreted as a guarantee of future outcomes. It has been prepared with care and objectivity to support long-term, planning-focused financial decisions.