Tax Saving Funds:Real Tax Saving, But Understand the Risks!

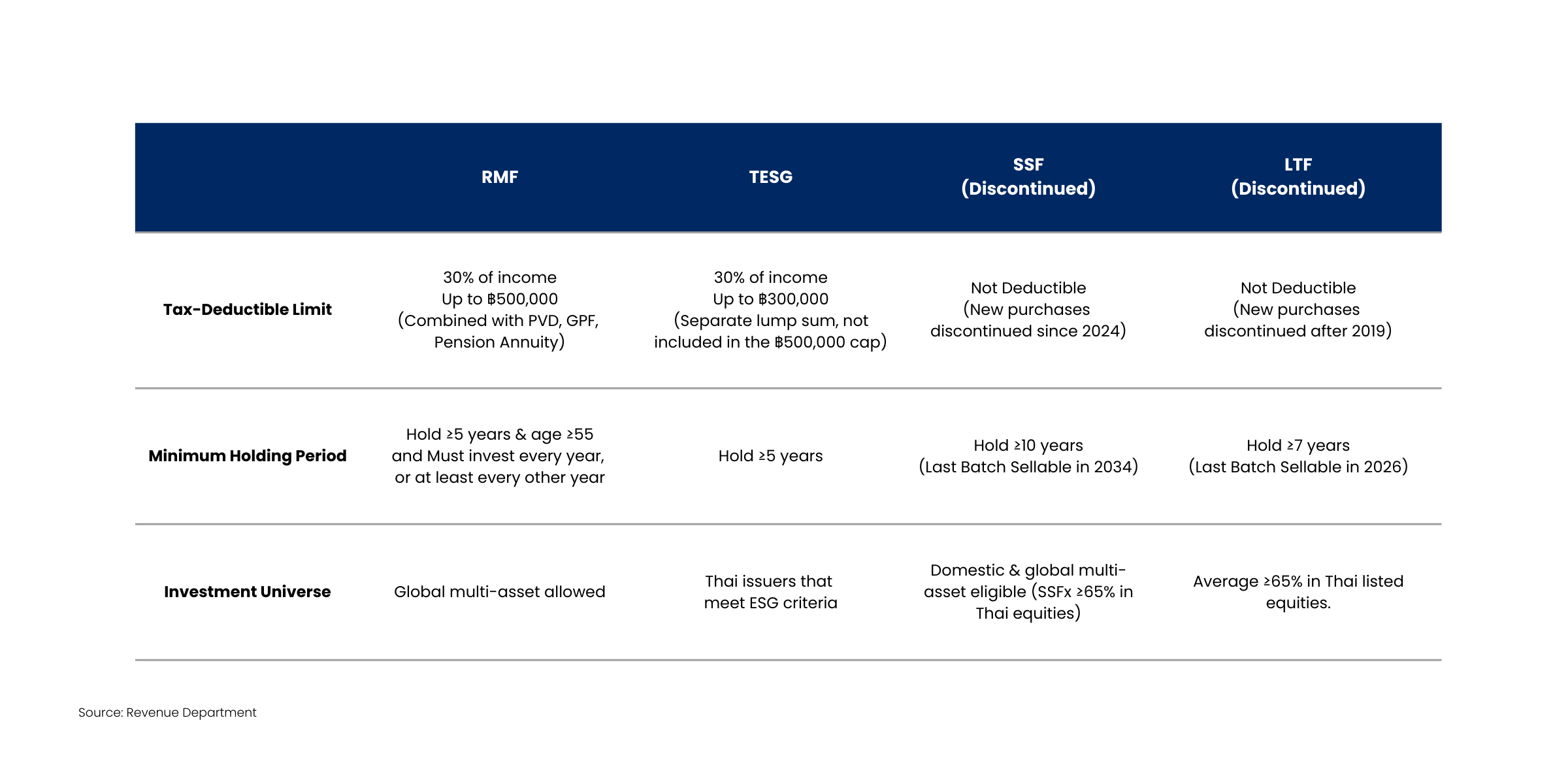

Every year, as the tax season approaches, investors rush to invest in tax-saving funds such as RMFs, ThaiESG funds, as well as LTFs and SSFs — both of which are no longer available for new tax-deductible investments but were once popular choices among investors seeking tax benefits. Many still view these funds as a sign of financial discipline and smart planning, combining the goals of reducing taxes and building long-term wealth.

Yet, the truth is that not every tax-saving fund leads to lasting financial success. Behind the promise of immediate deductions lie structural challenges that many overlook — restricted liquidity from holding requirements, country or sector concentration, and the performance volatility that comes with market-based investments.

The Allure of Tax Deduction Products

Tax-saving funds offer a rare combination of benefits: They help people save for their future and pay less tax now.. For many, this dual reward feels both practical and financially rewarding.

As with any investment, it’s important to remember that these products are still vehicles for generating returns, not just tools for tax deduction. Their performance and suitability depend on factors such as asset allocation, market conditions, and long-term objectives. When chosen thoughtfully, they can play a valuable role in building disciplined, goal-based portfolios.

That said, every investment product has its own characteristics and trade-offs. To make the most of tax-saving opportunities, investors should understand key features such as holding requirements and market exposure. With this understanding, tax efficiency becomes a complement to a sound investment strategy — not a substitute for one.

Hidden Risks Behind the Tax Benefits

While tax-savings funds offer genuine tax advantages, their underlying characteristics can introduce certain risks that investors may overlook. Recognizing these factors helps ensure that short-term tax savings work in harmony with long-term investment goals.

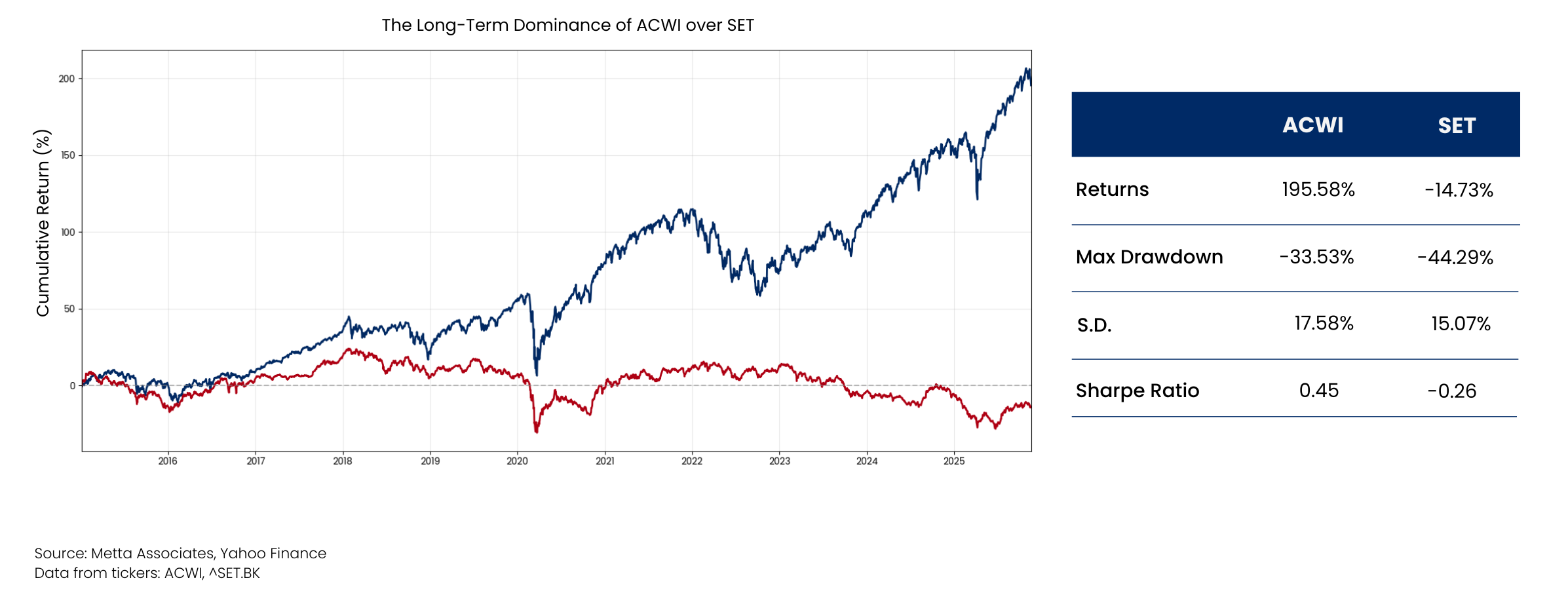

Concentration Risks When markets fluctuate, returns can vary sharply—especially if the fund invests in only a few countries or sectors, for example, ThaiESG funds which concentrate investments in Thai issuers. To see the real impact of investing in a single market, compare the performance of ACWI Index(representing the diversified global market) versus Set Index(representing the Thai market) below:

This clear difference in returns shows why limited diversification increases short-term risk and reduces stability. Understanding this helps investors set realistic expectations and fit tax savings funds properly into their overall portfolio.

Liquidity and Holding Constraints RMFs come with strict rules: investors must hold the investment for at least 5 years and be 55 years of age or older, and they must also invest continuously (at least every other year), making them suitable only for investors who are absolutely certain they won't need these funds until retirement and are comfortable with their money being locked in for an extended period, while ThaiESG and similar funds impose early-redemption penalties, including loss of tax benefits and required repayment of deductions. These rules reduce flexibility, making it harder to adjust when markets or personal needs change.

Behavioral Bias and Year-End Decision Pressure Near year-end, many investors rush to buy tax-saving funds mainly to claim deductions, often choosing products based on recent short-term performance or promotional offers. Morningstar has highlighted that indicators such as short-term returns or star ratings reflect only past performance and do not reliably predict future results. When investment choices are made under year-end pressure using these backward-looking signals, investors can become reactive and end up with decisions that do not align well with their long-term goals. A disciplined, fundamentals-based approach ensures that tax planning supports — not drives — investment choices. A disciplined, fundamentals-based approach ensures that tax planning supports — not drives — investment choices.

In essence, tax-saving funds can be valuable tools when used thoughtfully. By understanding their risks and limitations, investors can turn short-term tax advantages into sustainable, long-term gains — ensuring that every deduction truly contributes to financial well-being.

Key Takeaways:

Tax benefits should support — not replace — sound investing Tax Saving funds can be powerful tools for long-term savings, but investors should choose them based on financial goals and portfolio fit, not just for tax deductions.

Understand the trade-offs before you commit Holding restrictions, market volatility, and concentration risks — especially in funds that focus heavily on specific countries or sectors — can meaningfully affect portfolio stability and flexibility. Recognizing these structural limitations upfront helps investors use tax-saving products more wisely and sustainably.

Year-end investment pressure can impair decision quality The rush to secure tax deductions near year-end often leads investors to rely on backward-looking indicators such as short-term performance or promotional incentives. Proactive planning throughout the year helps mitigate these behavioral biases and supports more disciplined, fundamentally driven investment decisions.

Sources: Revenue Department, Yfinance

Metta Associates's Strategic Reflection

At Metta Associates, we believe effective tax planning is more than just claiming deductions. It’s about placing the right assets in the most suitable investment structures so they align with each client’s goals, risk tolerance, and financial path. This approach ensures that every investment decision serves a clear purpose — not only a tax advantage.

True financial growth comes from balance — where tax benefits work together with a well-built, thoughtful investment plan. By choosing suitable assets and focusing on steady, long-term results, we help clients turn short-term tax savings into lasting financial growth.

Disclaimer

This content is intended for general informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instruments. It does not consider your specific investment objectives, financial situation, or needs. You are encouraged to consult a licensed financial advisor before making any financial decisions.

The information presented is based on sources believed to be reliable; however, its accuracy or completeness cannot be guaranteed. This material does not represent a forecast and should not be interpreted as a guarantee of future outcomes. It has been prepared with care and objectivity to support long-term, planning-focused financial decisions.

Always with You.